The financial markets are witnessing a historic shift that extends far beyond typical cyclical fluctuations. In 2025, we’re experiencing what institutional investors are calling “the debasement trade”—a fundamental repricing of assets based on growing skepticism about the long-term stability of fiat currencies and the fiscal health of major economies. This isn’t merely another market trend; it’s a structural transformation that’s reshaping how capital allocates itself across the global financial system.

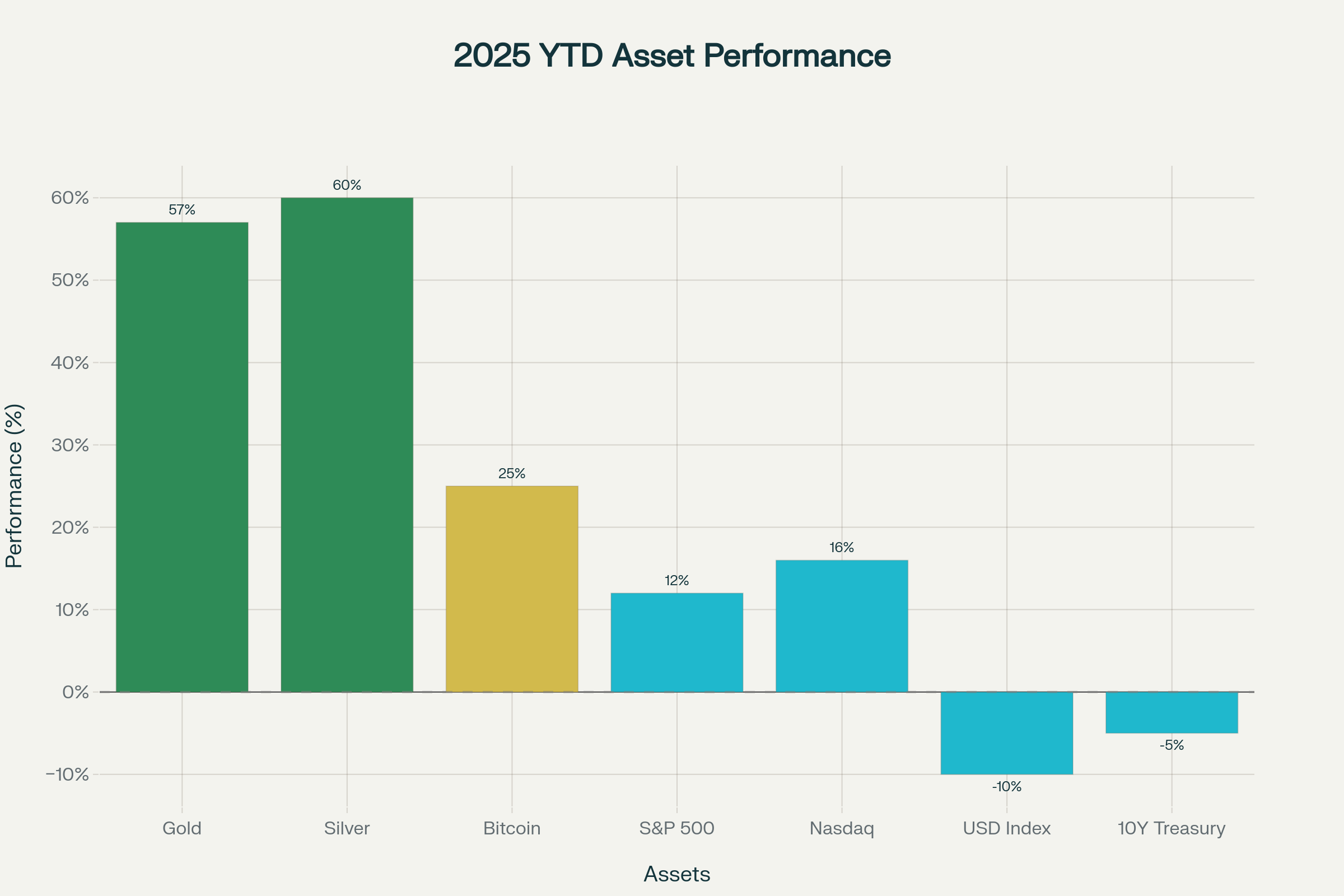

As gold soars past $4,100 per ounce for the first time in history, silver reaches heights not seen since 1980, and Bitcoin commands prices above $126,000, we’re witnessing more than speculative fervor. The numbers tell a compelling story: gold has surged 57% this year, silver 60%, while the U.S. Dollar Index has declined 10%—the steepest drop since the early 1970s. These aren’t isolated phenomena but interconnected symptoms of a deeper monetary crisis that’s forcing investors to fundamentally reconsider what constitutes true stores of value.

Understanding the Mechanics of Modern Debasement

Currency debasement, historically associated with ancient rulers diluting gold and silver coins with base metals, has taken on new forms in our modern financial system. Today’s debasement occurs through what economists term “fiscal dominance”—when government borrowing and monetary expansion systematically erode currency purchasing power faster than economic growth can justify.

The arithmetic is stark and undeniable. The U.S. federal debt has exploded to $37 trillion in 2025, up from $35.5 trillion just one year ago. More critically, the government now spends approximately $1 trillion annually on debt service alone—exceeding defense spending for the first time in modern history. This structural shift means that more than 14% of federal revenue now flows directly to creditors rather than productive government functions, creating a self-reinforcing cycle where higher interest rates exacerbate fiscal imbalances.

The M2 money supply expansion tells an equally concerning story. Since 2020, the U.S. money stock has increased by 36% while real GDP growth managed only 10%, indicating money creation far outpaced economic productivity. This divergence between monetary expansion and real economic output creates the fundamental conditions that drive the debasement trade.

The Federal Reserve’s Impossible Position

Federal Reserve officials find themselves navigating an increasingly precarious landscape where traditional monetary policy tools are being overwhelmed by fiscal realities. The September 2025 FOMC minutes revealed deep divisions among officials, with most supporting continued rate cuts despite inflation remaining persistently above the Fed’s 2% target. This represents a dramatic shift from the Fed’s historical mandate, as policymakers now must balance inflation control against the government’s growing debt service costs.

Real yields on 10-year Treasury Inflation-Protected Securities (TIPS) currently sit at 1.72%, while 10-year breakeven inflation rates hover around 2.30%. These figures suggest that even “inflation-protected” government securities offer minimal real returns when compared to the actual erosion of purchasing power experienced by consumers. The gap between official inflation statistics and asset price inflation has created a bifurcated economy where financial assets soar while real wages stagnate.

Central Banks Lead the Great Rotation

Perhaps no development better illustrates the debasement trade’s institutional legitimacy than central bank behavior. For the first time in nearly three decades, global central banks now hold more gold than U.S. Treasuries in their reserves. This represents a profound vote of no confidence in the dollar-denominated financial system that has anchored global commerce since Bretton Woods collapsed in 1971.

Central banks added a net 19 tonnes to global gold reserves in August alone, following years of record accumulation. The National Bank of Poland has emerged as the most aggressive buyer, significantly increasing its gold allocation, while institutions from Kazakhstan to El Salvador have joined the purchasing spree. China’s gold strategy exemplifies this systematic approach—the People’s Bank of China has added 316 tonnes since November 2022, while simultaneously reducing its Treasury holdings.

This isn’t merely prudent diversification; it’s a strategic repositioning for a multipolar monetary system. The World Gold Council’s 2025 survey revealed that 95% of central banks expect to increase their gold holdings over the coming years. When the world’s monetary authorities collectively pivot away from dollar-denominated assets, it signals structural rather than cyclical change.

The Institutional Embrace

The debasement trade has transcended its origins among gold bugs and cryptocurrency enthusiasts to become mainstream institutional strategy. Wall Street’s largest firms have not only endorsed the concept but actively marketed it to clients. JPMorgan coined the term in research notes, while analysts at Bank of America have raised their 2026 gold price target to $5,000 per ounce.

Institutional Bitcoin adoption has accelerated dramatically, with spot Bitcoin ETFs experiencing their strongest inflows since launch. Morgan Stanley’s decision to clear its 16,000 advisors to allocate client funds to cryptocurrency represents a watershed moment in institutional acceptance. Wells Fargo has followed suit, with UBS and Merrill Lynch expected to join shortly. These developments suggest the debasement trade has moved from fringe theory to core institutional strategy.

The data supports this institutional shift. Bitcoin ETFs have absorbed $22.5 billion through September 2025, with Bitwise predicting Q4 flows could surpass the record $36 billion set in the ETF’s inaugural year. BlackRock’s iShares Bitcoin Trust alone has attracted billions in institutional capital, while onchain data shows over 49,000 BTC withdrawn from exchanges by whale entities—indicating long-term accumulation rather than speculative trading.

The Fiscal Dominance Endgame

The concept of fiscal dominance—where monetary policy becomes subordinate to government financing needs—has moved from academic theory to market reality. Historical episodes of fiscal dominance, from Weimar Germany to modern-day Turkey, demonstrate how quickly monetary credibility can collapse when central banks lose independence.

President Trump’s escalating demands for Federal Reserve rate cuts have thrust this issue into public view, though Fed Chair Jerome Powell has publicly resisted political pressure. However, the mathematical constraints are becoming inescapable. With debt-to-GDP exceeding 120% and interest costs consuming ever-larger portions of the federal budget, the Fed faces an impossible choice: maintain monetary credibility at the cost of potential fiscal crisis, or accommodate government financing needs at the expense of currency stability.

The Congressional Budget Office projects that without significant fiscal adjustments, the U.S. debt-to-GDP ratio could exceed 170% within a decade under current trajectories. European analysis suggests the U.S. fiscal adjustment required to stabilize debt dynamics would need primary surpluses exceeding 3% of GDP—a level historically associated with debt crises.

Global Currency Alternatives Emerge

The debasement trade isn’t occurring in isolation but alongside systematic efforts to reduce dollar dependency in international commerce. The BRICS nations, now representing 45% of global population and 35% of world GDP, have accelerated development of alternative payment systems designed to bypass dollar-dominated infrastructure.

While a unified BRICS currency remains years away, incremental steps toward de-dollarization are accelerating. The Chinese renminbi now accounts for 50% of intra-BRICS trade, while bilateral currency swap agreements and central bank digital currency pilots are proliferating. Russia’s embrace of gold as a strategic asset following Western sanctions demonstrates how geopolitical tensions can accelerate monetary alternatives.

The dollar’s share of global foreign exchange reserves has declined to 58.4% in Q1 2025, down from approximately 71% in 2000. While this erosion appears gradual, it represents the most significant challenge to dollar hegemony since the currency’s emergence as the world’s reserve standard.

Asset Performance and Market Dynamics

The debasement trade’s market impact extends far beyond precious metals and cryptocurrencies. Copper has gained 26% in 2025 as investors seek exposure to industrial commodities with intrinsic value. Even equity markets have benefited, with the Nasdaq Composite up 19% and the Dow Jones Industrial Average gaining 9% as institutional liquidity flows into risk assets.

Real estate, art, collectibles, and other tangible assets have experienced similar appreciation as capital seeks inflation hedges. This broad-based asset inflation occurs even as official consumer price statistics remain relatively contained—highlighting the distinction between monetary debasement and conventional inflation measures.

The precious metals complex has led this rotation, with gold’s 45th record high of 2025 occurring in early October when prices first breached $4,000 per ounce. Silver’s performance has been even more dramatic, with the metal reaching $53 per ounce—levels not seen since the Hunt Brothers’ manipulation attempt in 1980. Analysts project silver could reach the $60s within the next year as industrial demand combines with monetary demand.

The Technology Factor

Bitcoin’s role in the debasement trade represents something qualitatively different from traditional inflation hedges. Unlike gold, which requires physical storage and has industrial applications, Bitcoin offers purely monetary properties with algorithmic supply constraints. Its fixed supply of 21 million coins provides mathematical certainty that no central authority can debase the currency through additional issuance.

The cryptocurrency’s recent volatility, including sharp declines from record highs above $126,000 to temporary lows around $104,000, reflects its continued price discovery process. However, institutional adoption and ETF inflows have provided structural support that didn’t exist in previous cycles.

Bitwise Chief Investment Officer Matt Hougan describes the debasement trade as “the dark matter of finance”—an invisible force affecting everything. This characterization reflects Bitcoin’s unique position as both a speculative asset and monetary technology, attracting capital from investors seeking both portfolio diversification and systemic hedge against fiat currency debasement.

International Perspectives and Regional Variations

The debasement trade isn’t confined to U.S. markets but reflects global concerns about fiscal sustainability across developed economies. Japan faces its own fiscal challenges with debt exceeding 250% of GDP, while France and the United Kingdom grapple with rising debt service costs and political instability.

German households demonstrate sophisticated understanding of fiscal dominance risks, with surveys showing that citizens who perceive limited fiscal space directly link higher debt expectations to increased inflation forecasts. This grassroots understanding of monetary dynamics suggests the debasement trade reflects genuine economic concerns rather than speculative mania.

European central banks have maintained their gold holdings at approximately 10,800 tonnes since 2020, reversing decades of net selling. The European Central Bank’s decision to halt gold sales and maintain substantial reserves signals institutional recognition of gold’s monetary role in an increasingly unstable financial system.

Investment Implications and Portfolio Construction

Traditional portfolio construction models—particularly the 60/40 stock-bond allocation—face existential challenges in a debasement environment. When both stocks and bonds can simultaneously underperform during periods of fiscal dominance, alternative allocations become necessary.

FxPro’s chief market analyst Alex Kuptsikevich recommends allocating approximately 20% of portfolios to alternatives including precious metals and cryptocurrencies, up from traditional allocations of 5-10%. This represents a fundamental shift in institutional thinking about portfolio construction and risk management.

The mathematics supporting alternative allocations are compelling. Gold has outperformed all major U.S. equity indices over one, three, and five-year periods, while providing negative correlation to stocks and bonds during market stress. Bitcoin, despite its volatility, has delivered superior long-term returns while offering exposure to a monetary system outside traditional financial infrastructure.

Real Yields and the Savings Destruction

Perhaps no metric better illustrates the debasement trade’s fundamental driver than real yields—the return on savings after accounting for inflation. Current 10-year TIPS yields of 1.72% provide minimal compensation for genuine purchasing power erosion, particularly when measured against asset price inflation rather than consumer price indices.

The phenomenon of negative real yields on government debt represents a historically unprecedented transfer of wealth from savers to borrowers—primarily governments. UK 30-year inflation-linked gilts currently offer -1.46% real yields, guaranteeing investors will lose one-third of their purchasing power over three decades. This represents what economists call “financial repression”—the systematic use of government policies to channel resources from private savers to public borrowers.

Market Structure and Systemic Risk

The debasement trade operates within market structures increasingly dominated by central bank intervention and government spending. Since 2020, fiscal deficits have become the primary driver of economic liquidity, superseding both private sector lending and traditional monetary policy transmission mechanisms.

This structural shift creates new systemic risks. When asset prices depend more on government spending than underlying economic productivity, market volatility can increase dramatically as fiscal policy changes. The government shutdown standoff in October 2025 provided a preview of how fiscal uncertainty can cascade through financial markets.

Professional investors increasingly recognize that traditional market analysis—focused on corporate earnings, economic growth, and monetary policy—must incorporate fiscal dynamics that were historically stable. This represents a fundamental change in how markets price assets and allocate capital.

The Path Forward

The debasement trade reflects more than investment strategy; it represents a monetary system in transition. Historical precedents suggest these transitions can extend over decades, with periodic crises accelerating change. The current environment shows characteristics of both the 1970s stagflation period and the monetary instability preceding the collapse of the Bretton Woods system.

Several scenarios could play out over the coming years. Optimistically, governments could implement credible fiscal consolidation programs that restore confidence in fiat currencies and allow traditional monetary policy to regain effectiveness. More pessimistically, continued fiscal deterioration could accelerate the debasement trade until it triggers a broader monetary crisis requiring systemic reform.

The most likely outcome involves continued gradual erosion of fiat currency purchasing power, punctuated by periodic crises that accelerate the rotation into hard assets. This environment favors investors who position portfolios for currency debasement while maintaining flexibility to adjust as conditions evolve.

Conclusion: The New Financial Paradigm

The debasement trade represents more than another investment theme—it signals a fundamental shift in how global capital perceives and prices monetary risk. When central banks accumulate gold at record rates, institutional investors embrace Bitcoin, and traditional portfolio allocation models prove inadequate, we’re witnessing the early stages of a new financial paradigm.

The mathematical constraints driving this transformation are becoming inescapable. With developed economy debt levels exceeding sustainable thresholds and central banks increasingly constrained by political pressures, the conditions supporting the debasement trade are likely to intensify rather than resolve. Investors who understand these dynamics and position accordingly may find themselves on the right side of one of history’s great wealth transfers.

The question isn’t whether the debasement trade will continue, but how quickly it will accelerate and which assets will prove most effective at preserving purchasing power in an environment of systematic currency erosion. For investors navigating this transition, the traditional rules of finance no longer apply—and the new rules are still being written by market forces bigger than any central bank or government can ultimately control.

As we move deeper into this monetary transition, one thing becomes clear: the debasement trade isn’t a short-term market phenomenon but a structural shift that will define investment strategy for years to come. Those who recognize this reality and adapt their portfolios accordingly may well find themselves positioned for the greatest wealth preservation opportunity in generations.