There are mining companies that look exciting on paper but struggle to deliver.

And then there are companies like Eldorado Gold in early 2026: not always flashy, sometimes overlooked, but increasingly hard to ignore.

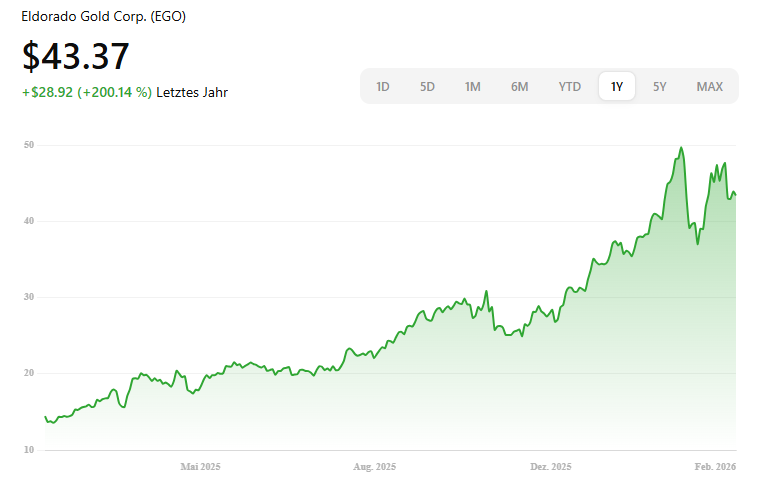

As of February 2026, Eldorado looks like a miner in transition — and in a meaningful way. The company has a solid operating base, improving financial strength, a notable run of exploration success, and a major growth project (Skouries) moving toward first production.

That doesn’t mean the story is risk-free. It isn’t. Skouries has seen a schedule push and added capital costs, and the company is still in a heavy spending phase. But that’s also what makes the current moment interesting: Eldorado’s existing mines are generating real cash while management pushes through the final stages of a transformational build.

If execution holds, 2026 could be the year Eldorado stops being viewed as “just another mid-tier gold producer” — and starts being valued as a broader gold-and-copper growth company.

Pull quote:

Eldorado’s core mines are doing the heavy lifting today while Skouries is being built for tomorrow.

A quick introduction: what Eldorado Gold actually owns

Eldorado Gold is a mid-tier mining company with assets in Canada, Türkiye, and Greece. Its portfolio includes producing gold mines, a polymetallic operation, and one large-scale copper-gold project under construction.

That geographic and asset mix matters. It gives the company:

current production and cash flow,

exploration upside across multiple districts,

and a visible pipeline for growth.

The most important facilities in the portfolio

Lamaque (Quebec, Canada) — the high-grade anchor

Lamaque is one of Eldorado’s standout assets and arguably the most strategically important operating mine in the portfolio. It combines established production with strong nearby exploration potential, which is exactly what miners want: a producing asset that may still have room to grow.

Recent drilling around Ormaque / Lamaque South reinforces the idea that Lamaque is more than a mature mine. It could remain a long-term value driver, especially if Eldorado advances plans to expand throughput toward higher permitted capacity.

Kisladag (Türkiye) — the volume contributor

Kisladag is one of Eldorado’s key production engines. It may not carry the same “high-grade excitement” as Lamaque, but it provides scale and helps support the broader business. In mining, steady volume matters — especially when a company is funding growth elsewhere.

Olympias (Greece) — valuable, but operationally demanding

Olympias is strategically important within Eldorado’s Greek portfolio because it offers gold production with polymetallic exposure. It also comes with more operating complexity, which has shown up in recent performance. The upside is there, but execution has to be tighter.

Efemcukuru (Türkiye) — smaller, steady, and useful

Efemçukuru is a smaller underground producer, but it remains an important contributor to group output and cash generation. These kinds of assets often don’t get headlines, but they help stabilize the portfolio.

Skouries (Greece) — the project that could redefine the company

This is the centerpiece of Eldorado’s growth story.

Skouries is a major gold-copper project under construction and the reason the company’s medium-term outlook looks different from its recent past. If ramped successfully, it should add scale, diversify revenue with copper, and reshape Eldorado’s production profile.

In simple terms: Skouries is the asset with the power to change the market’s perception of Eldorado.

The latest production data: steady delivery with a growth bridge forming

Eldorado’s latest reported results point to a company that largely did what it said it would do.

The headline number is strong: 2025 gold production reached 488,268 ounces, which landed at the high end of guidance. That matters because it shows the current operating base is still performing while management juggles a major project build.

Key production numbers (latest reported)

Q4 2025 gold production: 123,416 oz

FY 2025 gold production: 488,268 oz

FY 2025 gold sales: 491,204 oz

The portfolio wasn’t perfect on a mine-by-mine basis — some operations saw lower grades, recoveries, or operational constraints — but the overall result was still solid.

What that says about “yield”

If by yield we mean practical operating output and conversion into sellable ounces, the takeaway is this:

Eldorado’s production base remains reliable enough to hit targets,

but operational performance still varies across sites,

and the next step-change in overall yield likely depends on Skouries ramping on time and exploration wins converting into future mine plans.

That’s a very normal (and actually healthy) place for a growth-oriented miner to be.

Pull quote:

Eldorado is still a producer first — but for the first time in a while, the growth pipeline is beginning to look just as important as the current ounces.

Exploration: one of the strongest parts of the story right now

If you only follow Eldorado for quarterly production, you may be missing one of the most important developments in the company.

Its recent exploration update was genuinely encouraging.

The company reported high-grade results and extensions at key sites — especially Lamaque and Olympias — plus a new gold-copper skarn discovery at Stratoni in Greece. For a company already building a major copper-gold project, that kind of result adds strategic depth.

Why this matters (without the geology jargon)

Exploration results matter most when they are near existing infrastructure.

That’s because new high-grade zones near an operating mine or established district can potentially be turned into production more efficiently than a standalone greenfield discovery. In other words, the economics can be better, and the timeline can be shorter.

That is why Lamaque stands out. Eldorado isn’t just finding mineralization — it’s finding mineralization in a district that already matters.

Exploration spending is rising — and that’s a signal

Eldorado has guided 2026 exploration spending at $75–85 million.

That is not token spending. It suggests management believes the company has enough quality targets to justify continued investment. For investors, that usually signals confidence in the longer-term resource pipeline.

Skouries: still the main catalyst, still the main execution test

No Eldorado discussion in 2026 is complete without Skouries.

It remains both:

the company’s biggest opportunity, and

its biggest near-term execution variable.

Where Skouries stands (as of Feb. 2026)

The project is in advanced construction, and Eldorado has indicated:

first concentrate is expected in early Q3 2026 (after a roughly one-quarter delay),

commercial production is expected in Q4 2026,

and construction capital has increased by roughly $50 million from prior expectations.

That delay is not ideal. But it also doesn’t necessarily derail the story.

What matters now is whether Eldorado can finish the build and move through ramp-up without another significant stumble. If it does, Skouries could materially improve Eldorado’s production scale and cash flow mix.

Why Skouries changes the narrative

Historically, many investors have viewed Eldorado as a gold producer with decent assets and periodic operational variability.

Skouries introduces something different:

meaningful copper exposure,

larger potential production,

and a stronger multi-year growth profile.

That makes Eldorado potentially more interesting to both gold-focused and broader mining investors.

Pull quote:

Skouries is no longer just a long-dated promise. In 2026, it becomes an execution story.

Financials: stronger than the headline free cash flow number suggests

This is where the Eldorado story gets more nuanced — and arguably more attractive.

At first glance, reported free cash flow looks pressured. But that headline misses the real picture.

The core business is generating strong cash

Eldorado’s latest reported annual numbers show a company with robust underlying operations:

Revenue: $1.819 billion

Operating cash flow (continuing ops): $742.5 million

Adjusted EBITDA: $836.2 million

Net earnings (continuing ops): $519.9 million

Those are not the numbers of a company under operational strain.

So why does free cash flow look weak?

Because Eldorado is spending heavily on growth.

Total capital spending in 2025 was substantial, with a major portion going to Skouries construction. In other words, the company’s reported free cash flow is being pulled down primarily by a conscious investment decision — not by a weak operating base.

That distinction is critical.

It suggests Eldorado is in a temporary phase where:

the current mines are funding the business,

while growth capex depresses headline free cash flow,

ahead of a potential production and cash flow step-up after Skouries ramps.

Balance sheet and capital allocation: confidence is showing

Eldorado ended the year with a meaningful cash balance and manageable net debt for a company in the middle of a major build. Management has also moved to return capital to shareholders through:

share buybacks, and

a new dividend program.

That combination is notable. Companies that feel financially boxed in generally do not expand shareholder returns while still funding a large construction project.

Key Numbers Box (for easy scanning)

Eldorado Gold snapshot (latest reported, as of Feb. 2026)

2025 gold production: 488,268 oz (high end of guidance)

Q4 2025 gold production: 123,416 oz

2026 total gold production guidance: 490,000–590,000 oz (includes Skouries)

2026 Skouries guidance: 60,000–100,000 oz gold and 20–40M lbs copper

2026 exploration budget: $75–85M

2025 revenue: $1.819B

2025 operating cash flow (continuing ops): $742.5M

2025 adjusted EBITDA: $836.2M

Year-end cash: ~$869M

Debt: ~$1.275B

What to watch for next

Eldorado has momentum, but 2026 is not a “set it and forget it” year. It is a proof year.

The biggest things to watch

Skouries execution

Can Eldorado deliver first concentrate and commercial production on the updated timeline?

Do capital costs stay contained from here?

Operational consistency across the current mines

Strong portfolio results matter while Skouries is finishing construction.

Variability at individual sites is normal, but sustained underperformance would matter.

Exploration conversion

Great drill results are useful, but the market eventually wants to see them turn into mine plans, reserves/resources, and production value.

Cost discipline

Inflation, royalties, and operating cost trends will shape margins even in a stronger metal price environment.

Final take: a better story than the market may be giving it credit for

Eldorado Gold in February 2026 looks like a company with two engines:

a current engine (existing mines producing gold and cash flow), and

a future engine (Skouries + exploration + portfolio growth potential).

That is a powerful setup — if management executes.

The company is not without risk, and the Skouries timeline remains the key swing factor. But the broad picture is increasingly clear: Eldorado is building toward a larger and more diversified profile, and the underlying business appears strong enough to support that transition.

For a miner that often flies under the radar, that is exactly the kind of combination that can start to attract more attention.